Electricity forward prices moved higher across most National Electricity Market (NEM) states between early February and early March, while east coast gas markets continued to ease following relatively mild summer demand conditions.

The recent lift in electricity futures has coincided with rising geopolitical tension in the Middle East, which has injected additional uncertainty into global energy markets. While the direct link to Australian electricity fundamentals remains limited, the situation has contributed to a higher risk premium in forward markets.

Forward electricity pricing had remained relatively soft over the preceding months. The recent movement therefore appears less driven by structural shifts in domestic supply and demand, and more by heightened market sensitivity to global developments.

Below, we break down the key movements across electricity and gas markets and what they may mean for businesses managing procurement decisions.

⚡ Electricity Market

Forward electricity markets experienced a noticeable shift in sentiment through late February and early March, with retailers responding cautiously to recent futures volatility.

While the underlying spot market has remained relatively stable, forward pricing behaviour has become more reactive. Several retailers have withdrawn or repriced electricity offers during the period, and pricing validity windows have shortened considerably as retailers manage exposure to rapidly moving futures markets.

For businesses currently in market, this has translated into more challenging procurement conditions. Tender participation has been lower than usual, pricing validity periods are shorter, and offers may be withdrawn quickly if forward market movements continue.

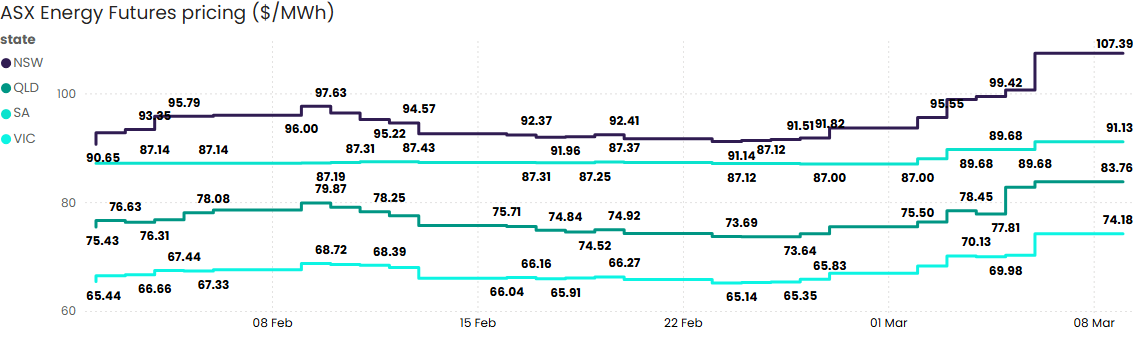

Source: ASX Energy Futures

New South Wales

NSW futures recorded the largest increase across the NEM, rising 18.5% from $90.65/MWh to $107.39/MWh. Prices trended steadily upward through the period, reaching the highest trading level at the close and trading within a range between $90.65/MWh and $107.39/MWh.

The sharp increase reflects a rising risk premium in the forward market as traders respond to global energy uncertainty.

Queensland

QLD futures increased 11.0%, closing at $83.76/MWh after opening at $75.43/MWh. The market traded within a $73.64/MWh to $83.76/MWh range, indicating moderate volatility but a clear upward trajectory across the period.

Queensland remains particularly sensitive to shifts in forward market sentiment given its large generation fleet and strong exposure to export-linked energy dynamics, which can amplify price movements during periods of global uncertainty.

South Australia

South Australia recorded the smallest change across the NEM, with futures rising 4.6% from $87.14/MWh to $91.13/MWh. Prices traded within a relatively narrow band between $87.00/MWh and $91.13/MWh, reflecting comparatively stable market conditions.

South Australia’s generation mix continues to play a role in moderating forward price volatility. High renewable penetration, strong interconnection with Victoria and increasing battery capacity provide additional system flexibility, supporting relatively stable pricing expectations compared with other eastern states.

Victoria

Victoria futures rose 13.4%, increasing from $65.44/MWh to $74.18/MWh. Trading remained within a contained range between $65.14/MWh and $74.18/MWh, suggesting steady upward sentiment rather than extreme volatility.

Despite the increase, Victoria continues to sit at the lower end of the NEM pricing curve, reflecting relatively strong supply conditions and ongoing renewable generation contribution across the region.

Western Australia

Wholesale electricity prices in WA showed moderate volatility between February and mid-March. Daily average prices generally ranged between $60/MWh and $110/MWh, with most trading days remaining within this band.

A notable price spike occurred on 2 February, when the maximum price reached $900/MWh, pushing the daily average to $176.80/MWh, the highest level during the period. The market also experienced occasional negative minimum prices, indicating periods of oversupply or strong renewable generation during low demand intervals.

🔥 Gas Market

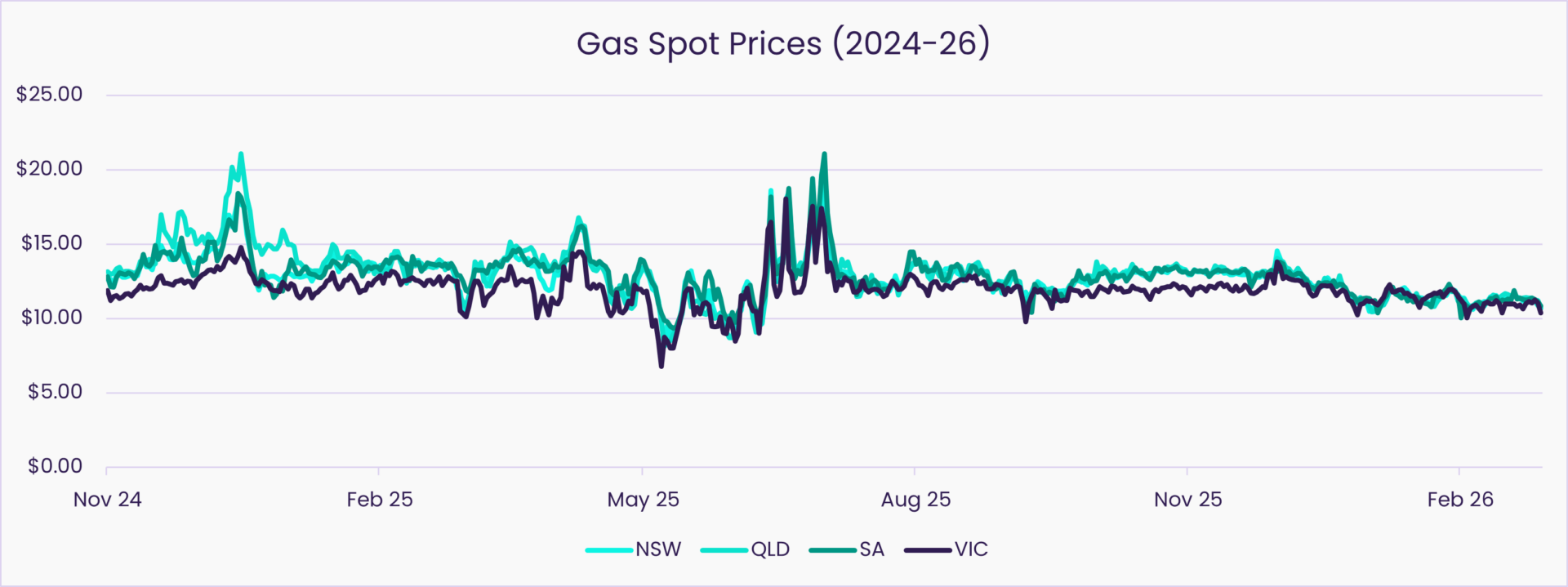

East coast gas markets continued to soften through the December–February period, with all major states recording year-on-year price declines.

The easing trend reflects milder summer demand conditions and improved supply availability compared with the previous year. While global gas markets have become more sensitive to geopolitical developments, east coast spot markets have remained relatively stable through the summer period.

Source: AEMO STTM and DWGM

New South Wales

Gas spot prices in NSW declined across the summer period, falling from $12.37/GJ in December 2025 to $11.27/GJ in February 2026, representing an 8.85% decrease.

On a year-on-year basis, prices were also lower across each month, with declines ranging from 14.23% to 16.74%, indicating softer market conditions compared with the previous summer.

Queensland

Queensland experienced the largest price correction across the east coast, with prices decreasing from $12.45/GJ in December to $11.25/GJ in February, a 9.66% decline across the period.

Year-on-year movements were also significantly lower, particularly in December where prices fell 23.63%, reflecting improved supply availability and weaker seasonal demand.

South Australia

South Australian prices softened from $12.36/GJ in December to $11.15/GJ in February, marking a 9.84% decline over the summer period.

Year-on-year comparisons also showed notable decreases, with prices falling between 13.25% and 18.11%, highlighting subdued gas market conditions across the region.

Victoria

Victoria experienced a more moderate decline, with prices moving from $11.99/GJ in December to $10.89/GJ in February, representing a 9.20% fall.

Year-on-year declines ranged between 5.05% and 13.30%, suggesting comparatively stable pricing relative to other east coast markets.

🌏 LNG Netback

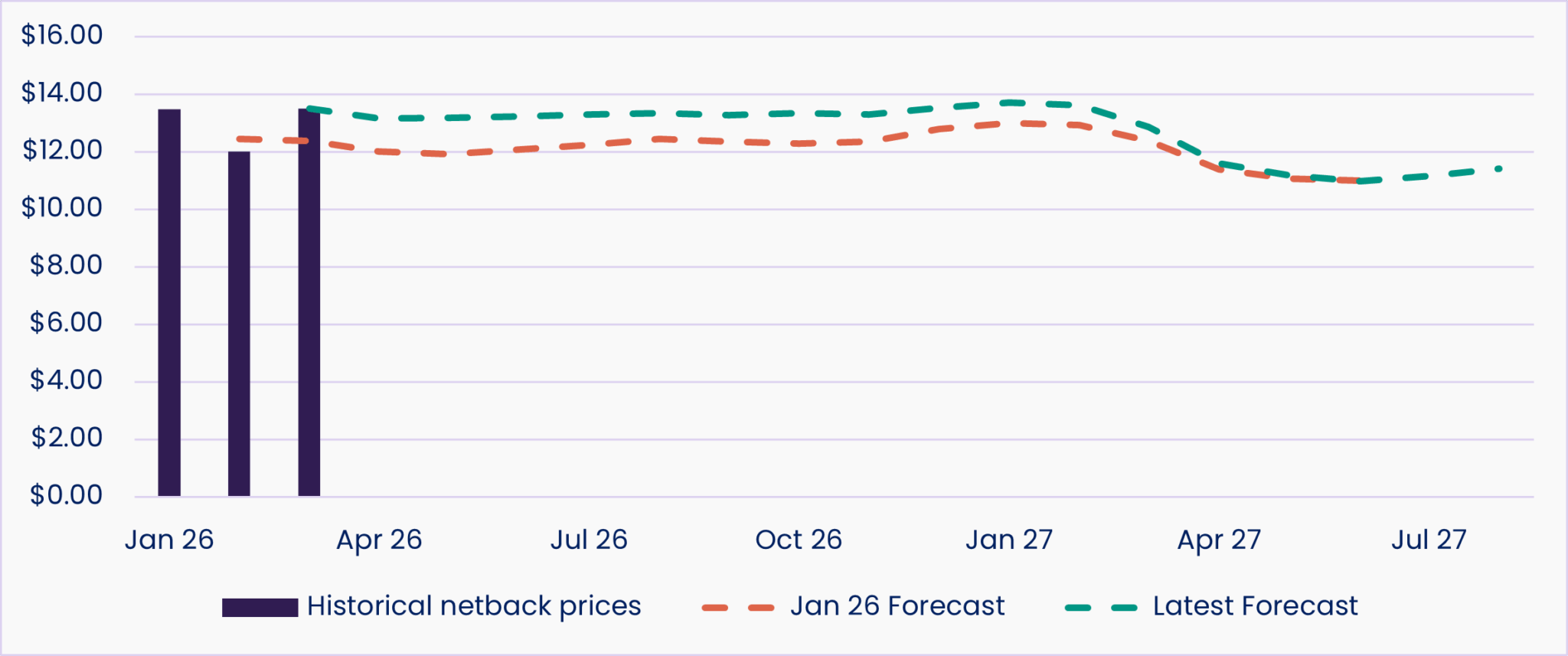

LNG netback forecasts have shifted higher across the 2026 forward curve, reflecting tightening global gas market sentiment.

The March 2026 netback forecast increased from $12.37/GJ to $13.50/GJ, while forecasts across April to December 2026 have been revised upward to approximately $13.15–$13.53/GJ, compared with the $11.9–$12.8/GJ range expected in the January outlook.

As discussed earlier, recent global developments have added further uncertainty to international energy markets, contributing to the upward revision in forward LNG pricing expectations. For Australian businesses, LNG netback remains a key reference point for east coast gas pricing given the link between export markets and domestic contract negotiations.

Further along the curve, forecasts suggest prices may gradually ease through 2027, declining from approximately $12.85/GJ in March 2027 to around $11–$11.9/GJ by 2028 as additional global LNG supply enters the market.

👀What We’re Watching

Forward Market Sensitivity to Global Events

Recent geopolitical developments highlight how quickly sentiment can shift in forward electricity markets. While underlying spot market conditions remain relatively stable, global uncertainty is feeding into forward pricing behaviour and retailer risk management.

For businesses entering the market, this is translating into shorter pricing validity periods, reduced retailer participation and more reactive pricing movements. Monitoring how quickly forward markets stabilise will be important for procurement timing decisions over the coming months.

Global LNG Signals and Domestic Gas Pricing

While east coast gas spot markets have remained relatively soft through the summer period, movements in global LNG expectations continue to influence forward pricing signals.

What we are watching is how LNG netback indicators evolve over the coming months, particularly if global market uncertainty persists. These signals will remain an important reference point for domestic gas contract negotiations.

📚 Further Market Context

Recent reporting has highlighted the broader global backdrop influencing energy markets. Rising oil prices linked to Middle East tensions are being watched closely as a potential inflation risk, while analysts have also pointed to the sensitivity of global LNG supply chains and shipping routes to geopolitical developments.

For readers interested in the wider context, the following sources provide useful perspectives.

- ABC – Strikes on Iran throw spanner in the works for inflation as oil price surges

- ABC – Attack on Iran could drive up Australia’s power prices

- Australian Financial Review – Gold and oil stocks cushion ASX as Iran conflict weighs

- The Guardian – Australian energy bills could surge as Iran conflict drives up global gas prices

- ACCC – Gas Inquiry 2017-30 – LNG Netback Price Series

- AEMO – Quarterly Energy Dynamics – Q4 2025

Frequently Asked Questions

How do geopolitical events influence Australian energy markets?

Geopolitical events can affect global oil, gas and LNG markets, which in turn influence pricing signals used in Australian energy contracts. Even when local supply conditions remain stable, global uncertainty can lead to higher risk premiums in forward markets and increased pricing volatility.

Why are electricity forward markets reacting to events in the Middle East?

While Australia’s electricity system is largely driven by domestic supply and demand, global developments can still influence market sentiment. When geopolitical tensions increase uncertainty in global energy markets, traders often incorporate additional risk premiums into forward electricity pricing.

Could Middle East tensions increase Australian energy prices further?

Direct supply impacts on Australia are limited, but global oil and LNG markets are closely interconnected. If geopolitical tensions disrupt key energy supply routes or push global fuel prices higher, those changes can flow through to Australian energy markets via international gas pricing and broader market sentiment.

The extent of any impact will depend largely on how long tensions persist and whether they affect major shipping routes or production infrastructure. Energy markets tend to react quickly to uncertainty, but pricing impacts often stabilise once supply risks become clearer.

Why are gas markets softer while electricity futures are rising?

East coast gas spot markets have remained relatively stable due to milder summer demand and improved supply conditions. Electricity forward markets, however, are reacting more quickly to global developments and changes in risk sentiment, which can drive short-term divergence between gas and electricity price signals.

Why are retailers shortening pricing validity periods right now?

Periods of increased forward market volatility make it more difficult for retailers to manage pricing risk. As a result, retailers may shorten pricing validity periods or withdraw offers more quickly to limit exposure if futures markets move rapidly.