October delivered another month of steady pricing across the NEM, with futures holding in tight ranges and renewables continuing to shape daytime conditions. Strong rooftop solar and favourable wind kept pressure off wholesale prices, while gas markets remained stable in the low-to-mid teens.

Here’s a clear snapshot of the key trends that defined October:

⚡ Electricity Market

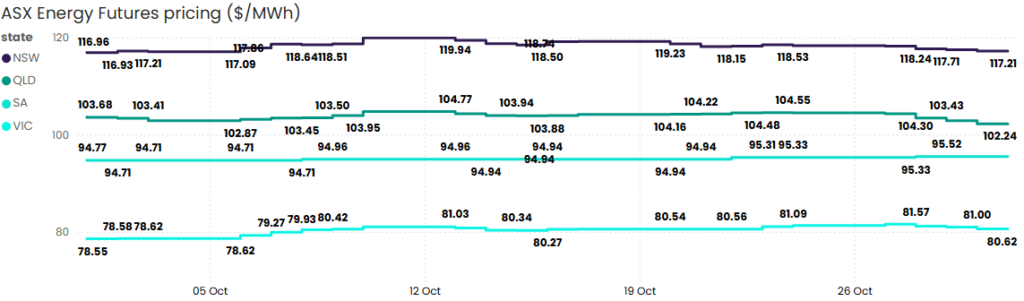

Source: ASX Energy Futures

Overall, October futures were steady across most NEM regions, with modest movements and limited volatility. Renewables continued to shape daytime pricing, but futures largely reflected stable forward expectations.

New South Wales

NSW futures were stable across October, trading between $116.93/MWh and $119.94/MWh. The contract closed at approximately $117.21/MWh, almost unchanged from the start of the month. Trading ranges remained tight, indicating subdued volatility and steady demand conditions. Mild temperatures and strong daytime solar kept pressure off the forward curve.

Queensland

QLD futures eased slightly through the month, starting at $103.68/MWh and finishing at $102.24/MWh. Prices ranged from $102.87/MWh to $104.77/MWh, consistent with Queensland’s typical spring stability. Strong rooftop solar and high daytime renewable penetration helped keep futures contained, despite short evening peaks on warmer days.

South Australia

SA futures exhibited the lowest volatility across the NEM once again, holding between $94.71/MWh and $95.52/MWh for virtually the entire month. The contract ended October at $95.52/MWh, less than a dollar above where it began. Strong wind output and frequent daytime negative pricing underpinned the stability of forward pricing.

Victoria

VIC futures saw moderate strengthening through October, rising from $78.55/MWh to a closing level of $80.62/MWh. Prices ranged from $78.55/MWh to $81.57/MWh, reflecting mild volatility compared to other regions. Consistent wind conditions and strong rooftop solar kept spot prices soft, but forward curves edged higher in anticipation of summer demand.

Western Australia

October spot conditions remained broadly stable in the South West Interconnected System (SWIS). The WA market continues to be supported by thermal generation, with renewables influencing daytime pricing without materially shifting forward expectations.

Tasmania

Tasmanian futures were broadly steady across October, with limited volatility reflecting the state’s strong reliance on hydro and relatively mild seasonal demand. Hydro inflows remained sufficient to support stable generation, and interconnector conditions with Victoria were generally favourable. Pricing movements were minimal, consistent with Tasmania’s typical spring pattern of low variability and strong renewable availability.

New Zealand

In New Zealand, October electricity prices remained relatively subdued across most regions. Strong hydro storage levels and favourable inflows supported sustained generation, while wind conditions were generally consistent with seasonal averages. Mild temperatures kept demand contained, contributing to month-long stability. The market continues to track toward a soft end to the year, with reservoir levels playing a key role in shaping forward expectations.

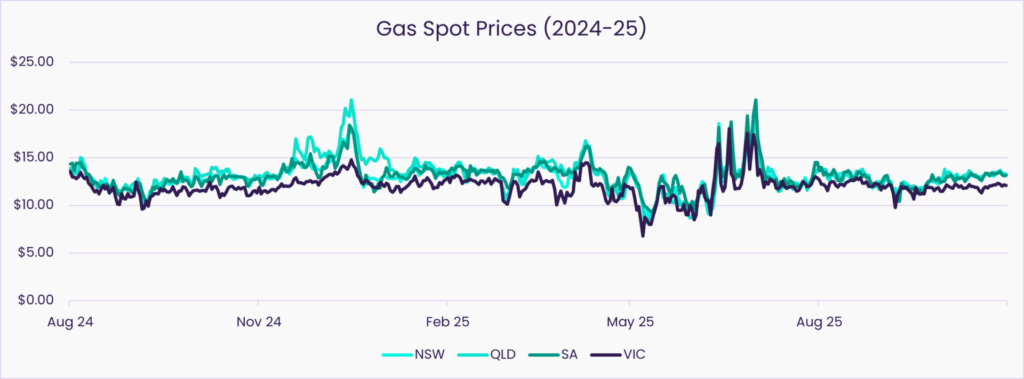

🔥 Gas Market

Source: AEMO STTM and DWGM

Gas spot prices remained in the low-to-mid teens across all hubs through August–October, with limited deviation and no major volatility events. The charts show a consistent band just above $10/GJ through October, supported by mild weather and steady supply.

New South Wales

NSW prices increased from $11.99/GJ in September to $12.93/GJ in October, a 7.8% month-on-month rise. Year-on-year prices for October were 1.17% higher. Despite the lift, prices remain within a stable range relative to earlier in the year.

Queensland

QLD prices rose from $12.28/GJ to $13.28/GJ, up 8.2% month-on-month. Year-on-year movement was relatively flat (–0.18%), continuing Queensland’s trend of being the most stable gas hub on the east coast.

South Australia

SA prices increased from $12.03/GJ to $12.77/GJ, up 6.1% month-on-month. SA’s year-on-year uplift for October was more pronounced at 2.18%, although overall pricing remains aligned with long-term spring averages.

Victoria

VIC prices rose from $11.26/GJ in September to $11.60/GJ in October, a 3.0% increase. Victoria saw a year-on-year uplift of 3.23% for October, supported by consistent winter-to-spring supply conditions and moderated storage withdrawals.

LNG Netback

LNG netback prices softened through October, easing from the mid-teens to $12.43/GJ as at 31 October. This continues the downward shift from earlier in the year, when netbacks were holding closer to $16–$17/GJ. While January 2025 forecasts had expected Q4 prices to remain above $20/GJ, the latest outlook reflects moderating global demand and more balanced supply conditions.

Record Renewables Push Daytime Operational Demand to New Lows

AEMO data shows renewables reached new heights through October, with strong rooftop solar and favourable wind conditions driving daytime demand to some of the lowest levels recorded across the NEM. Several regions experienced extended periods where renewable output met the majority of grid requirements, contributing to more frequent daytime curtailment and negative wholesale prices. The trend highlights how quickly supply dynamics are shifting as spring conditions amplify renewable availability.

What does this mean for you?

• For large energy users: increasing opportunity to optimise or shift processes into low-cost daytime windows.

• For procurement teams: renewables-driven volatility reinforces the need to understand load shape when evaluating contracts.

• For corporates: curtailment and renewable timing risks are becoming more relevant to PPA performance and net zero planning.

More Retailers Explore Daytime ‘Three for Free’ Offers as Solar Surges

October saw more retailers pilot or launch free or ultra-low-cost daytime energy deals for households and small businesses, driven by strong rooftop solar and regular midday oversupply. These offers reflect a structural shift in market conditions as solar penetration reshapes demand curves and pushes wholesale prices down in the middle of the day. We covered this emerging trend in our recent LinkedIn article on “three for free” energy offers, unpacking why retailers are shifting their product design and what it signals for the broader market. While still targeted at smaller customers, the shift signals how retailers are responding to the changing supply curve.

What does this mean for you?

• For commercial and industrial users: tariff structures and contract options may evolve as daytime oversupply becomes more common.

• For energy managers: the shift reinforces the value of demand flexibility and building operational alignment with low-price periods.

• For strategy teams: retailer activity is an early indicator of how commercial offerings may adapt as solar continues to grow.

Australia Reaches Clean-Energy Milestone as Renewables Outpace Fossil Generation

New national data shows October marked a turning point: monthly renewable generation slightly exceeded fossil-fuel output across the eastern states for the first time. Strong wind and solar contributed to the result, supported by mild weather and stable system conditions. The milestone underscores the pace of transition and highlights the growing role of variable generation in determining forward market expectations.

What does this mean for you?

• For businesses: long-term procurement strategies need to account for deeper renewable penetration and evolving firming requirements.

• For investors: increasing renewable dominance elevates the importance of storage, hybrid assets and flexible technologies.

• For corporate buyers: contract structures may need reviewing to ensure they remain aligned with changing generation patterns.

If you would like to understand how these trends relate to your business, your contracting position or your broader energy strategy for 2026 and beyond, Utilizer is here to help. Our team monitors these movements daily so you can navigate the market with clarity and confidence, backed by data and practical guidance.

Reach out if you would like to discuss your portfolio, explore optimisation opportunities or review upcoming renewal windows.

More power to you.